Executive Summary

Why this matters now

The Global Risks Report 2026, published by the World Economic Forum, marks a clear inflection point in how global risks are perceived and prioritized. For the first time in more than two decades, geoeconomic confrontation — rather than war or climate — is identified as the most likely trigger of a material global crisis in the immediate term.

According to the Global Risks Perception Survey (GRPS) 2025–2026:

- 18% of respondents selected geoeconomic confrontation as the top risk for 2026, ahead of state-based armed conflict at 14%

- 50% of leaders expect a turbulent or stormy global outlook over the next two years, rising to 57% over the next decade

- Technological risks (misinformation, cyber insecurity, adverse AI outcomes) move decisively into the short-term risk stack

- Environmental risks are reprioritized downward in the short term, yet dominate severity rankings over the 10-year horizon

This paper translates those findings into operational and strategic implications for:

- Supply Chain & Logistics leaders

- Trade and Customs professionals

- Manufacturing and industrial operations

- Foreign direct investment and nearshoring strategies in Mexico

Current Global Risk Landscape – Top risks most likely to trigger a global crisis in 2026

1. Introduction: operating in the “Age of Competition”

The WEF defines the current period as the “Age of Competition” — a phase in which trade, finance and technology are increasingly deployed as tools of strategic leverage rather than neutral market instruments.

Rules and institutions that historically underpinned global stability are under strain. Multilateral coordination is weakening, while unilateral and regional actions are becoming the norm. The result is not a clean break from globalization, but a fragmented, contested operating environment where risk travels faster and compounds across systems.

For supply chains, this means that volatility is no longer a disruption scenario; it is the baseline.

Short-term (2-year) and long-term (10-year) global outlook

2. Methodology: how the risk signals are generated

The Global Risks Report 2026 is grounded in the Global Risks Perception Survey (GRPS), which gathered input from more than 1,300 experts across business, government, academia, international organizations and civil society.

Key methodological features:

- Risks are assessed across three time horizons: 2026, 2028 and 2036

- Respondents evaluate likelihood, severity and interconnections between risks

- Results are complemented by the Executive Opinion Survey, capturing national-level risk perceptions from business leaders in 116 economies

This matters because the report does not attempt to forecast a single future. Instead, it maps plausible trajectories, showing how risks cluster, reinforce each other and cascade across systems — a critical lens for supply chain design.

3. The 2026 risk stack: what rises to the top now

3.1 Geoeconomic confrontation: the dominant short-term risk

In 2026, geoeconomic confrontation becomes the number one global risk, moving up two positions from last year. The report describes an expanding use of:

- Tariffs and trade controls

- Sanctions and investment screening

- Subsidies and state aid

- Restrictions on technology, capital and critical inputs

These tools are increasingly justified on national security grounds, accelerating economic fragmentation.

For supply chains, this translates into:

- Policy-driven disruptions rather than demand-driven shocks

- Higher exposure to sudden regulatory shifts

- Increased compliance and sourcing complexity

3.2 Trust breakdown: misinformation and societal polarization

Two societal risks stand out in the 2026 rankings:

- Societal polarization (#4, 7%)

- Misinformation and disinformation (#5, 7%)

The report links these risks to weakening institutional trust, volatile policy-making and impaired crisis response. For global trade and logistics, this creates an environment where perception can move faster than fundamentals, affecting investment sentiment, labor stability and regulatory direction.

3.3 Technology risk moves into the operational core

2026 introduces two new technological risks into the Top 10:

- Adverse outcomes of AI technologies (#8, 4%)

- Cyber insecurity (#9, 3%)

While technological acceleration drives productivity, the report highlights growing exposure of critical infrastructure, supply chain platforms and data flows to cyber incidents and AI-related misuse.

In practical terms, cyber risk is no longer an IT issue — it is a business continuity and trade execution risk.

4. Two horizons, two different risk profiles

One of the most important insights of the 2026 report is the divergence between short-term and long-term risk priorities.

- Short term (2 years): dominated by geoeconomic, geopolitical and societal shocks

- Long term (10 years): environmental risks reclaim dominance in severity

By 2036, the top risks by severity are:

- Extreme weather events

- Biodiversity loss and ecosystem collapse

- Critical change to Earth systems

Global risks ranked by severity – 2-year vs 10-year horizon

5. Risk interconnections: why disruptions cascade

The report’s interconnections map shows inequality as the most interconnected global risk for a second consecutive year.

Inequality amplifies:

- Societal polarization

- Political instability

- Weaker institutions and rule of law

- Economic nationalism and trade friction

These dynamics create risk cascades, where social stress translates into policy shifts, which then disrupt trade flows and supply chains.

6. Sector impact analysis

6.1 Supply Chain & Logistics

- Network design must treat policy and regulatory risk as structural constraints

- Redundancy and optionality gain importance relative to pure cost efficiency

- Visibility, data integrity and scenario planning become core capabilities

6.2 Global Trade & Customs

- Non-tariff barriers and enforcement intensity increase

- Trade compliance, origin management and data accuracy become strategic assets

- Errors carry higher financial and reputational costs

6.3 Manufacturing

- Shift away from extreme just-in-time models

- Regional supplier development becomes a strategic investment

- Closer integration between plants and logistics partners

7. Mexico, nearshoring and foreign direct investment

The Report 2026 does not single out Mexico as a country case. However, its core findings — particularly the rise of geoeconomic confrontation, the retreat of multilateralism and the growing use of economic tools for strategic leverage — directly reshape the investment logic behind nearshoring to North America.

Mexico remains structurally relevant to global manufacturers and investors. What has changed is the criteria by which Mexico is evaluated.

Nearshoring decisions in 2026 are no longer driven primarily by labor cost arbitrage or proximity alone. They are increasingly framed as risk allocation decisions.

7.1 Nearshoring under geoeconomic confrontation

From efficiency play to risk hedge

For nearshoring investors, Mexico’s relevance stems from three structural advantages in this environment:

- Geographic proximity to the U.S. market, reducing exposure to long, politically sensitive supply routes

- Deep trade integration under USMCA, which partially shields flows from broader global fragmentation

- Established manufacturing and logistics ecosystems, particularly in automotive, electronics, appliances and industrial goods

However, geoeconomic confrontation also introduces new investor questions:

- How exposed is the operation to sudden tariff or regulatory shifts?

- Can the supply chain remain compliant under tighter enforcement and scrutiny?

- How resilient is cross-border logistics under political or social stress?

7.2 Installed foreign investment: recalibration, not retreat

One of the most important implications of the Global Risks Report for Mexico is what it does not suggest: a generalized withdrawal of foreign capital.

Instead, the report points to strategic recalibration:

- Investors reassess footprint design

- Capital deployment becomes more phased and conditional

- Resilience metrics gain weight alongside ROI

For companies already operating in Mexico, this typically translates into:

- Greater focus on operational continuity rather than rapid expansion

- Internal diversification across regions within Mexiconal continuity rather than rapid expansion

- Internal diversification across regions within Mexico

- Increased scrutiny of energy reliability, security and logistics infrastructure

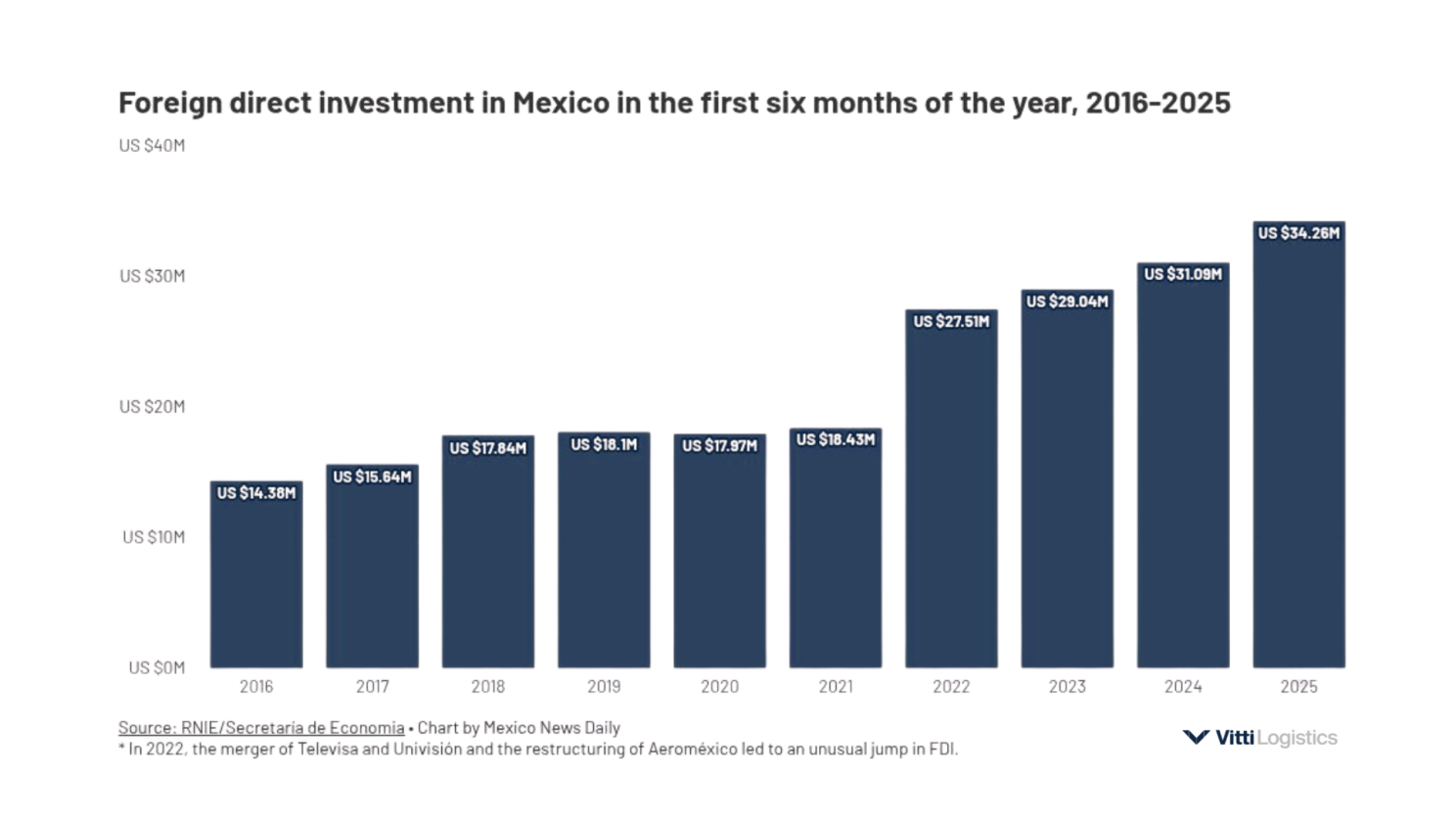

In a world where 50% of global leaders expect a turbulent short-term outlook, capital deployment favors resilience over speed — a pattern visible in Mexico’s sustained, but more selective, FDI inflows

7.3 Policy risk and regulatory visibility as investment variables

The Global Risks Report emphasizes the erosion of trust in institutions and the weakening of multilateral frameworks. For nearshoring investors, this shifts attention from headline incentives to policy execution and predictability.

In Mexico, this manifests in three critical areas:

- Trade and customs enforcement As geoeconomic confrontation intensifies, enforcement — not just regulation — becomes the primary risk channel.

- Industrial and energy policy clarity Investors increasingly model scenarios around regulatory stability rather than assuming continuity.

- Rule of law and contract reliability Societal polarization and institutional strain — both highlighted in the report — translate into higher perceived operating risk.

These factors do not negate Mexico’s attractiveness, but they raise the threshold for due diligence and risk pricing.

7.4 Supply chain design implications for nearshoring projects

The report’s emphasis on risk interconnections — particularly inequality, polarization and infrastructure stress — has direct implications for how nearshored supply chains are designed in Mexico.

Key shifts observed among investors and manufacturers:

- Moving away from single-site concentration toward networked regional footprints

- Integrating logistics providers earlier in investment planning

- Designing inventory buffers as strategic options, not inefficiencies

Logistics is no longer treated as a downstream function. It becomes a risk-management layer between production and market access.

7.5 What sophisticated nearshoring investors are doing differently in 2026

Based on the Global Risks 2026 signals, leading investors are:

- Treating nearshoring as a portfolio strategy, not a single-country bet

- Embedding geopolitical and regulatory risk into supply chain modeling

- Elevating trade compliance, data integrity and cyber resilience as board-level concerns

- Selecting logistics and 3PL partners based on risk governance capabilities, not price alone

Mexico benefits when it is positioned not just as a manufacturing location, but as part of a managed, resilient North American supply system.

7.6 Closing perspective for investors

The Global Risks Report 2026 describes a world where competition replaces coordination and resilience replaces optimization as the primary objective.

In that world, Mexico’s role in nearshoring is not diminished — it is redefined.

The decisive question for investors is no longer “Can we manufacture closer to market?” It is “Can we operate, comply and deliver reliably under sustained geopolitical and economic pressure?”

Mexico remains central to that answer — for those prepared to design for risk.

8. Strategic recommendations for supply chain and trade leaders

Based directly on the 2026 risk signals:

- Embed geoeconomic risk into network design and S&OP Treat tariffs, sanctions and controls as recurring variables, not exceptions.

- Upgrade trade compliance from cost center to control tower Classification, origin and data governance reduce disruption risk.

- Extend cyber requirements across logistics partners TMS, WMS, EDI and 3PLs are part of the attack surface.

- Stress-test Mexico–US corridors against climate and policy shocks Extreme weather dominates long-term severity rankings.

- Invest in verified risk intelligence Misinformation and polarization distort decision-making faster than traditional indicators.

Strategic takeaway – Vitti VGPT

The Global Risks Report 2026 does not point to a distant horizon. It describes the operating conditions supply chains are already navigating.

In this Age of Competition, resilience is no longer a defensive buffer. It has become a strategic capability — one that shapes investment decisions, supply-chain design and long-term competitiveness.

Vitti Global Pulse of Trade (VGPT) provides executive-level insight on geopolitics, trade policy, and supply chain risk — translating complexity into operational clarity for North American businesses.

➡️ Subscribe to our newsletter and follow us for updates on the webinar date—don’t miss the insights that will shape the future of global trade.