Executive Brief

January 2026 opens with a clear signal for global operators: tariffs are no longer episodic political events — they are recurring operating variables.

Two dynamics are shaping the current trade environment:

- Growing tariff complexity in the United States, driven by overlapping legal authorities such as IEEPA, Section 232, and Section 301, often with cumulative effects on landed cost and compliance risk.

- The use of tariffs as geopolitical leverage, illustrated by a public threat to impose escalating duties on imports from multiple European allies unless a political agreement is reached — a move widely covered and challenged by international counterparts.

For companies operating across U.S.–Mexico supply chains, the primary risk is no longer simply “higher tariffs,” but volatility, timing uncertainty, scope ambiguity, and execution risk.

1. IEEPA and Section 232: How the U.S. Tariff Framework Is Evolving

Recent guidance from U.S. Customs and Border Protection (CBP), combined with ongoing legal and policy developments, confirms a fundamental shift in how U.S. tariffs are being designed and applied.

In 2026, the U.S. tariff framework is no longer defined by a single instrument or a linear escalation model. Instead, it is shaped by the overlapping use of emergency powers, national security authorities, and reciprocal measures, each with distinct scopes, exclusions, and enforcement mechanics.

IEEPA: Emergency Powers and Legal Uncertainty

The Congressional Research Service (CRS) confirms that the U.S. administration has increasingly relied on the International Emergency Economic Powers Act (IEEPA) to impose tariffs tied to non-traditional trade issues, including migration, drug trafficking, and broader national security concerns.

Several of these actions remain under active legal challenge, creating uncertainty around:

- duration and permanence,

- enforceability,

- and the potential for partial rollbacks, pauses, or replacement mechanisms.

Executive implication: Tariffs imposed under IEEPA carry higher volatility risk than traditional trade remedies. Finance, pricing, and contracting teams should assume change scenarios, not static duty rates, when modeling exposure.

Section 232: Sector-Based Measures with Expanding Reach

Alongside IEEPA, Section 232 (national security) tariffs continue to play a central role in U.S. trade policy, particularly across:

- automotive and auto parts,

- steel, aluminum, copper,

- timber and lumber,

- and medium- and heavy-duty vehicles.

Unlike traditional trade remedies, Section 232 actions can be expanded, modified, or re-scoped through presidential proclamations, often with limited transition periods.

What CBP’s latest guidance clarifies

CBP’s most recent tariff overview highlights a critical operational reality for importers:

Tariff exposure is no longer uniform — and tariffs do not always stack automatically.

Key clarifications include:

- Certain products subject to Section 232 (autos, auto parts, MHDVs) are explicitly excluded from additional IEEPA tariffs.

- Other products remain exposed to multiple tariff authorities, depending on classification and origin.

- Drawback eligibility varies by tariff type and country, directly affecting duty recovery and cash flow.

- Products containing mixed metal content may still face multiple Section 232 duties simultaneously, depending on composition thresholds.

This reinforces a central takeaway for leadership teams:

Tariff risk in 2026 is a product-level governance issue, not a country-level assumption.

Why this matters for U.S.–Mexico supply chains

For companies operating across U.S.–Mexico corridors — particularly in automotive, industrial manufacturing, and nearshoring-driven networks — this evolving framework introduces three immediate risks:

- Cost distortion Headline tariff rates may materially understate true landed cost.

- Contractual exposure Fixed pricing agreements may not reflect conditional or changing tariff applicability.

- Compliance and execution risk Incorrect assumptions around tariff stacking increase the likelihood of post-entry corrections, penalties, and clearance delays.

What leaders should do now

- Reassess tariff exposure SKU by SKU, not by country alone

- Validate HTS classifications, material content, and origin assumptions

- Align trade, finance, and procurement teams around scenario-based costing

🔗Official reference: https://www.cbp.gov/sites/default/files/2026-01/factsheet_2025_post_trade_summit_v.36.pdf

CBP – U.S. Tariff Overview: IEEPA and Section 232 (January 2026)

2. Tariffs as Geopolitical Leverage: When Trade Policy Becomes Conditional

Recent developments surrounding Greenland offer a clear illustration of a broader shift affecting global trade and supply chain planning in 2026: tariffs are increasingly being used as conditional leverage rather than traditional trade remedies.

In January, President Trump publicly outlined the possibility of escalating tariffs on imports from multiple European countries, linking market access explicitly to the outcome of negotiations related to Greenland. While the political debate has been highly visible, the more relevant signal for business leaders lies in how trade policy is being framed — not in the geopolitical dispute itself.

Market signal vs. policy reality

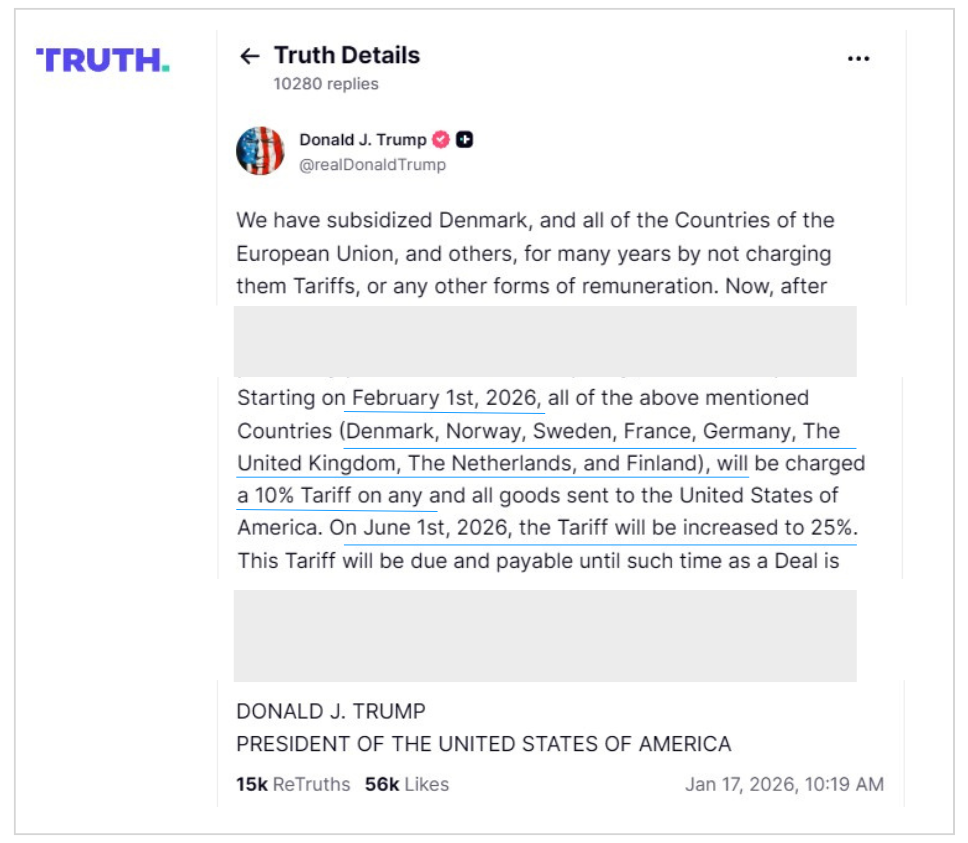

The proposed tariff escalation — 10% beginning February 1, 2026, rising to 25% on June 1, 2026 — was communicated through a public post on President Trump’s Truth Social account.

It is critical to clarify that, as of this publication, these proposed measures:

- have not been formalized through an Executive Order or Presidential Proclamation,

- have not been published in the Federal Register,

- and have not been implemented or operationalized by U.S. Customs and Border Protection.

Public social media statement referencing potential tariff measures. As of publication, no formal trade action has been issued through official U.S. channels.

From a compliance standpoint, no enforceable trade action currently exists.

From a business standpoint, however, the announcement still matters.

Public, conditional tariff statements — even when issued outside formal regulatory channels — function as market signals. They influence expectations, shape risk perception, and introduce uncertainty into commercial decision-making well before any legal mechanism is activated.

A shift toward conditional trade policy

Unlike conventional tariffs grounded in dumping, subsidies, or industry injury, the Greenland-related tariff threat reflects a different logic:

- Broad scope: applying across all goods rather than targeted sectors

- Conditional application: linked to political outcomes, not trade behavior

- Predefined escalation: with future rate increases tied to negotiation timelines

This signals a move away from purely rule-based trade enforcement toward a more transactional model, where tariffs are positioned as tools within a broader negotiation framework.

For global companies, this blurs the traditional boundary between trade compliance and geopolitical risk management.

Implications for global and North American supply chains

Even without formal implementation, the announcement has immediate second-order effects on global trade planning:

- Tariff volatility becomes a planning variable Companies importing into the U.S. from Europe face uncertainty unrelated to product characteristics or supply-demand dynamics, complicating pricing and margin forecasting.

- Contractual friction increases Conditional tariffs undermine long-term agreements that assume stable tariff frameworks, forcing companies to revisit escalation clauses, force majeure language, and risk-sharing mechanisms.

- Acceleration of supply chain reconfiguration Firms may expedite diversification or nearshoring decisions — not for cost efficiency, but to reduce exposure to policy-driven volatility.

For North America, the impact is indirect but material. As tariffs are used as leverage even against long-standing allies, the relative attractiveness of regionalized supply chains increases. Mexico, in particular, may see heightened demand for manufacturing and assembly capacity as companies seek political and geographic proximity to the U.S. market.

At the same time, this environment raises the bar for trade governance. When tariffs can be announced, escalated, or withdrawn rapidly and conditionally, resilience depends less on tariff optimization and more on structural flexibility and decision speed.

Executive takeaway

The Greenland episode reinforces a central reality for 2026:

Tariffs are no longer only corrective trade instruments — they are bargaining tools that introduce volatility even before they exist in law.

For senior leaders, the critical question is no longer “Will this tariff be implemented?” It is “Are our supply chains designed to operate under conditional and rapidly shifting trade signals?”

Organizations that continue to treat tariffs as static inputs risk mispricing, margin erosion, and operational disruption. Those that integrate policy signaling into trade and supply chain strategy will be better positioned — regardless of how individual negotiations ultimately resolve.

3. U.S.–China: The Realignment Signal Behind 2026 Supply Chains

A decade-long evolution of U.S.–China trade policy shows how tariffs and non-tariff measures have shifted from episodic actions to a structurally persistent framework — setting the stage for today’s supply chain realignment

Trade flows between the United States and China are sending a clearer message than policy headlines: the global supply chain is being re-priced, re-routed, and re-allocated — and the shift is proving durable.

A 2025 analysis from project44 points to one of the sharpest year-over-year contractions in bilateral goods trade in decades: U.S. imports from China fell 28%, while U.S. exports to China declined 38%. Whether measured through customs data, carrier networks, or capacity deployment, the direction is consistent: trade friction is translating into structural redistribution of manufacturing and shipping patterns.

1) Trade is shrinking — but the network is adapting, not freezing

Project44’s report also highlights a critical nuance for operators: while volumes weakened, ocean networks adjusted quickly. It notes that blank sailings fell to 62 in December from a peak of 131 in April, signaling carriers have rebalanced capacity and routing for the new demand reality.

This matters because it suggests we are not dealing with a temporary disruption. We are watching a managed reconfiguration: fewer China-origin moves, more triangulation via alternative origins, and network redesign to protect margins.

2) Diversification is accelerating — Southeast Asia is capturing share

The same project44 findings point to a clear beneficiary set: Southeast Asian economies are absorbing an increasing share of U.S.-bound trade, with Indonesia (+34%) and Thailand (+28%) singled out as growth markets in U.S. imports during 2025.

For global manufacturers, this is the practical definition of “China+1” moving from strategy deck to operating model:

- new supplier qualification cycles,

- multi-country BOM redesign,

- and shifting lead-time risk from a single mega-corridor to a portfolio of lanes.

3) Tariffs and non-tariff constraints are now a combined cost stack

What changed in 2025 is not only tariff levels — it is the stacking of instruments: tariffs, reciprocal adjustments, and non-tariff constraints such as licensing and export controls. This increases compliance friction and makes “lowest cost” sourcing less relevant than lowest volatility sourcing.

Public data and policy trackers show 2025 included periods of exceptionally high tariff pressure, followed by later-year stabilization at lower effective levels — reinforcing that volatility itself is now part of the cost equation.

Executive takeaway: 2026 planning must treat tariffs as dynamic, not static, and integrate legal/policy uncertainty directly into scenario costing.

4) Beyond Tariffs: The Instruments Reshaping U.S.–China Trade in 2026

While tariffs continue to influence trade flows, the defining feature of U.S.–China commercial relations in 2026 is instrument-level friction — policies that affect how, when, and whether goods and technologies can move across borders.

These measures are less visible than headline tariffs, but often more disruptive for supply chains.

Export controls and licensing regimes The U.S. Department of Commerce, through the Bureau of Industry and Security (BIS), has confirmed case-by-case licensing requirements for exports of advanced semiconductors and related technologies to China.

Operational impact: Even in the absence of new tariffs, companies face longer compliance timelines, licensing uncertainty, and cascading effects on manufacturing schedules and capital deployment.

Section 301 and logistics-related equipment Recent actions under Section 301 reference maritime and logistics-related equipment, including port and cargo-handling infrastructure.

Why this matters for North America: As nearshoring accelerates, China-origin components are more likely to pass through Mexican operations before entering the U.S., increasing the importance of re-export controls, origin transparency, and documentation discipline.

5) The demand backdrop: early 2026 remains soft — and policy clarity is the missing input

Shipping demand into the U.S. is expected to remain below year-ago levels into spring. The National Retail Federation projects January 2026 container volumes at 2.11 million TEUs, still 5.3% lower YoY, with the first YoY increase not expected until May.

NRF’s framing is notable: retailers are not only adjusting to demand cycles — they are explicitly seeking greater stability and certainty around tariffs and trade policy to support smoother operations in 2026.

What this means for North America (U.S.–Mexico lens)

For North American supply chains, the U.S.–China realignment creates a dual outcome:

- Nearshoring opportunity expands As firms diversify production footprints, Mexico becomes more attractive for final assembly, regional distribution, and time-sensitive supply chains.

- Complexity shifts, it doesn’t disappear When components still originate in Asia, Mexico-based manufacturing must strengthen:

- origin governance,

- HTS accuracy,

- supplier documentation discipline,

- and lead-time resilience across multiple lanes.

Executive takeaway

The U.S.–China lane is no longer the singular backbone of global trade growth. It is becoming a managed corridor — smaller, more regulated, and more volatile.

For leadership teams, the winning posture in 2026 is not predicting headlines. It is building supply chains that can operate under:

- shifting tariff regimes,

- mixed policy signals,

- and a network where capacity and sourcing re-balance faster than annual planning cycles.

What Leaders Should Act on Now

January 2026 reinforces a critical reality for global operators: trade policy has shifted from a background constraint to an operating variable. Tariffs, non-tariff tools, and policy signaling are now moving faster than traditional planning cycles — and the cost of slow reaction is rising.

What this means for leadership teams

Finance & Pricing

- Recalculate landed-cost scenarios assuming tariff stacking, conditional measures, and volatility, not static rates

- Align customer and supplier contracts with duty-adjustment and re-pricing mechanisms

Trade Compliance

- Conduct a rapid audit of HTS classification, origin, and valuation for top-margin SKUs

- Establish a clear policy-change response playbook with defined decision rights and timelines

Procurement & Sourcing

- Accelerate dual-sourcing and diversification for tariff-sensitive or policy-exposed inputs

- Validate supplier readiness for export controls, licensing, and documentation discipline

Operations & Logistics

- Review Incoterms, duty-payer responsibilities, and inventory buffers under stress scenarios

- Stress-test cross-border flows for disruption, rerouting, and lead-time variability

VGPT Action Checklist (10-Day Sprint)

- ☐ Top 20 SKUs by margin mapped to HTS, origin, and tariff exposure

- ☐ Tariff authority matrix (IEEPA / 232 / 301) per product family

- ☐ Contract clauses covering duty volatility

- ☐ Internal escalation process for tariff changes

- ☐ Validation with customs broker and fiscal advisors

Closing Insight

The defining challenge of 2026 is not predicting the next headline — it is building organizations that can operate under persistent policy uncertainty.

For companies across U.S.–Mexico supply chains, competitive advantage will increasingly depend on governance, visibility, and response speed, not just cost efficiency. Those that integrate trade policy signals into financial, sourcing, and operational decisions will be better positioned to navigate a structurally more complex global trade environment.

Vitti Global Pulse of Trade (VGPT) provides executive-level insight on geopolitics, trade policy, and supply chain risk — translating complexity into operational clarity for North American businesses.

About Vitti Logistics

Vitti Logistics is a growing North American 3PL provider specializing in tech-driven, customized supply chain solutions. Our expanding “blue footprint” signifies our commitment to delivering reliable warehousing, transportation, and value-added services where industry thrives.

🌐 Learn more: www.vittilog.com

➡️ Subscribe to our newsletter and follow us for updates on the webinar date—don’t miss the insights that will shape the future of global trade.